Economic and Market Commentary by Aziz Meherali

The US-Iran conflict and the closure of the Strait of Hormuz, which we wrote about in our last quarter newsletter, has still not been resolved and the news out of Washington doesn’t align with news out of Tehran creating further uncertainty and increases risk of escalation.

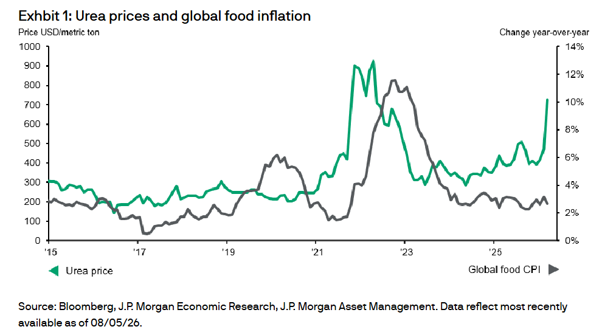

The Strait of Hormuz is not only a passageway for oil but also for bulk commodities and 20% of global fertilizers as well. Ukraine was also a significant producer of fertilizers and the war in that region saw food prices soar. This issue in Iran is a double whammy as it is not only fuelling food price inflation but energy price inflation as well. Keep in mind, there is a lag on the effect of prices as what we are paying today was sourced some months ago, so we are yet to see the higher prices and impact of shortages.

This has started to cause spillover effects from energy prices to cost of goods and services, potentially impacting on global growth. Off course, the contagion effects vary country to country and diversification of exposure once again presents risk mitigation as well as opportunities for the longer-term investor.

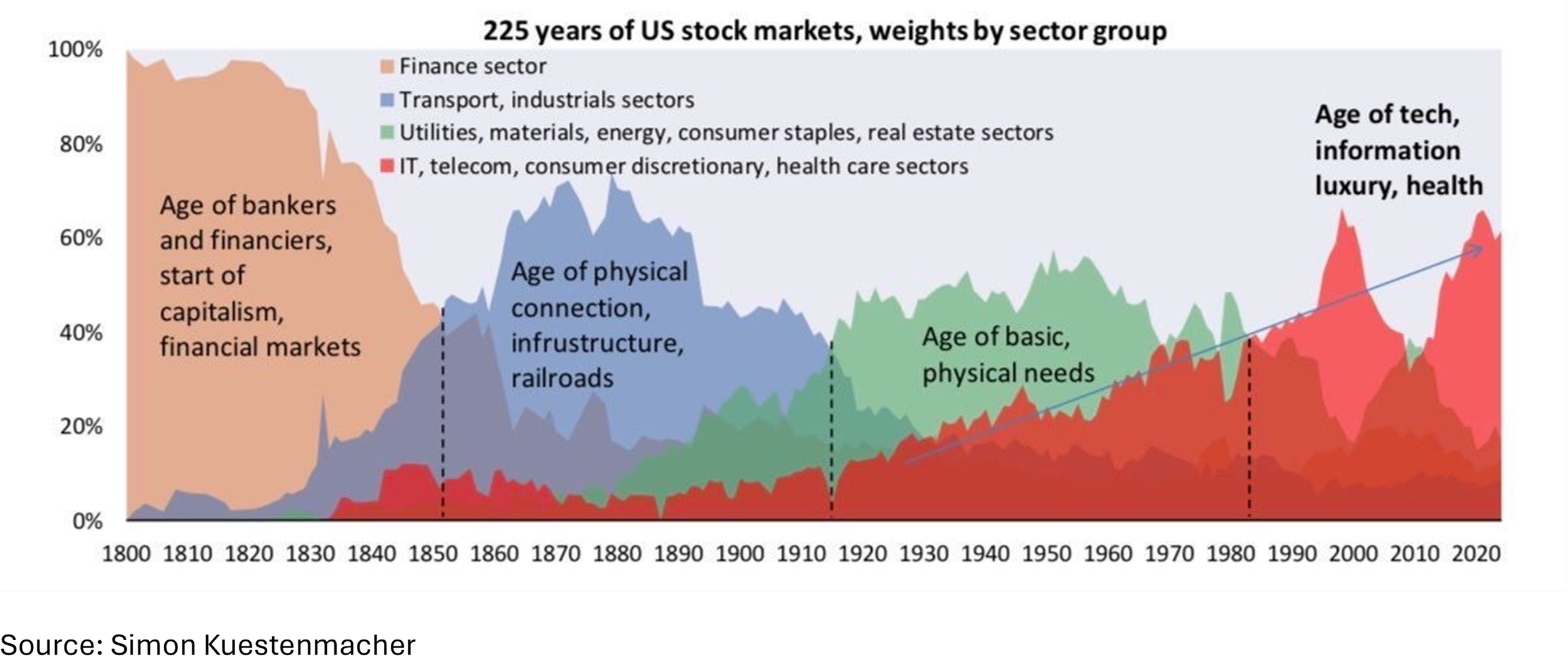

Markets focussed on AI and less reliant on energy imports are likely to be more resilient and continue to provide growth opportunities versus those economies heavily reliant on energy import and lacking access to AI exposure in their economies. As you can see from the chart below, we are in the age of AI:

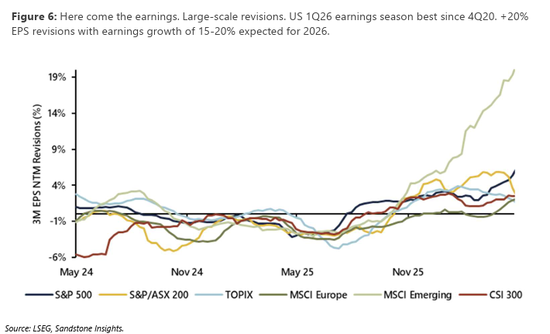

When we look at the most recent reporting season gone past in the US, earnings revisions have been on the upside and in double digits. In the Q1 2026 reporting season, the S&P 500 posted a stellar earnings season with a blended (year-over-year) earnings growth rate of roughly 28.4%. A massive 84% of S&P 500 companies beat EPS estimates, reporting an aggregate earnings surprise of 18.2% above expectations.

The surge was largely driven by an infrastructure investment boom in Artificial Intelligence (AI) and strong earnings from tech bellwethers.

However, Australia remains an outlier being heavily dependent on energy imports and having a small to no AI industry. This is likely to be further exacerbated by the Federal Budget presented recently by our treasurer, Jim Chalmers. There is a distinct lack of focus on productivity growth and no beneficial tax reform to drive that productivity that can eventually translate into higher economic growth.

This further highlights the need to have overseas exposure in our portfolios and a tilt towards those areas that present growth opportunities which also helps to mitigate downside risks.

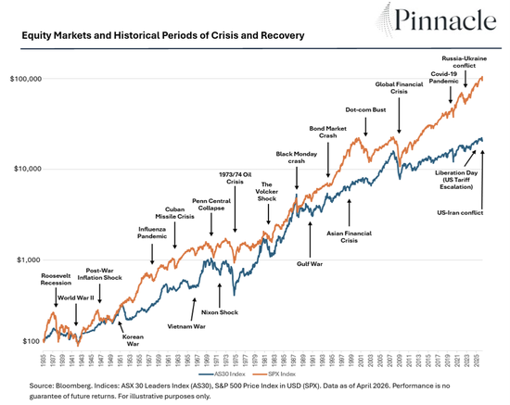

With every crisis that we have been witness to since the early 1900s and most recently the 2009 (GFC), 2022(covid), 2025 (Nov—AI investment concerns), and 2026 (Feb-oil shock concerns), there are always opportunities that need to be uncovered. Our brains are wired to have ‘loss aversion’ where a loss in financial wealth is felt much more negatively than the same positive impact of the same size. Furthermore, social media seems to amplify bad news.

At Elixir Private Wealth, we tend to take a longer-term view of markets and also tend to be contrarian by nature. We look at the macro environment through proprietary research from financial stalwarts such as JP Morgan and Blackrock, to name a couple. We then ascertain where there might be opportunities from a regional perspective, and also on the opportunities within each industry and employ this knowledge to better shield our portfolios, and position them to avail the opportunities that present themselves in a volatile environment whilst still remaining steadfast to the longer-term, strategic asset allocation for our clients.

Patience is key to withstanding volatility as is clearly illustrated in the chart below. Human endeavour is what the share market is a proxy for and that is focused on positive returns and outcomes in the long run.

Here are a few quotes that hopefully will provide some food-for-thought in these volatile times:

“ The true investor welcomes volatility …a wildly fluctuating market means that irrationally low prices will periodically be attached to solid businesses” –Warren Buffett

“ When one door closes, another opens; but we often look so long and so regretfully upon the closed door that we do not see the one which has opened for us” ---Alexander Graham Bell